Know Your Customer (KYC) verification is a mandatory compliance process on most reputable Indian betting sites, designed to confirm players’ identity, age, residential address, and the legitimacy of their funds. In India, operators typically require documents such as a PAN card or Aadhaar for identity proof, utility bills or bank statements for address verification, and bank account or UPI details to validate payment methods and sources of income. These checks align with national anti-money laundering (AML) frameworks and help sites meet Reserve Bank of India (RBI) guidelines when processing rupee transactions.

Proper KYC not only ensures regulatory compliance but also unlocks faster withdrawals, higher betting limits, and enhanced account security. Conversely, skipping or delaying verification can lead to frozen winnings, account restrictions, or exposure to unlicensed platforms with weaker dispute resolution. While some low-KYC or no-KYC betting options exist—often offshore or cryptocurrency-based—they carry significant risks, including sudden account freezes and limited legal recourse. This guide walks you through the entire Indian KYC process, from gathering the right documents to troubleshooting common rejections, and provides a balanced look at alternative verification pathways.

Understanding KYC On Indian Betting Sites

KYC in online gambling refers to the process of collecting and verifying a player’s personal information to establish identity, confirm legal age (18+ in most Indian states), validate residency, and comply with anti-money laundering regulations. Indian betting platforms use KYC to cross-check submitted data against government databases and financial records, ensuring the person registering is who they claim to be and meets eligibility criteria.

At the point of signup, most sites collect basic profile details: full name as it appears on official ID, date of birth, residential address, mobile number, and email. More sensitive verification—uploading scanned copies of Aadhaar cards, PAN cards, or voter IDs—often occurs later, triggered either by the platform’s onboarding flow or automatically when a player initiates a withdrawal. Some operators also request additional proof when cumulative deposits or withdrawal amounts exceed specified thresholds, aligning with RBI transaction-monitoring norms.

Timing varies by operator. Many require partial KYC (name and phone verification via OTP) immediately after registration to prevent duplicate or underage accounts. Full document-based verification is commonly deferred until the first withdrawal request, though proactive submission right after account creation helps avoid delays when you want to cash out winnings. Understanding this two-stage model—basic profile data first, comprehensive document review later—can streamline your experience and reduce friction at critical moments.

Why Indian Betting Sites Need KYC

The primary objectives of KYC are to prevent underage gambling, combat identity fraud, satisfy AML obligations, and minimize payment chargebacks. By verifying that every user is at least 18 years old and holds genuine government-issued identification, operators protect vulnerable individuals and shield themselves from legal liability. Anti-fraud measures extend to cross-checking submitted documents against known forgery patterns and flagging accounts with inconsistent information.

To achieve these goals, betting platforms employ database cross-checks—comparing Aadhaar or PAN numbers with official registries—and biometric or selfie-based verification. Selfie uploads, often requiring a player to hold their ID next to their face, serve as liveness checks that confirm the person onboarding matches the photo on the submitted document. Advanced systems may use facial recognition algorithms to detect manipulated images or deepfakes, adding an extra layer of security.

AML compliance is particularly critical for sites handling Indian rupee deposits and withdrawals. Under RBI guidelines, financial institutions and payment processors must maintain detailed records of high-value transactions and report suspicious activity. Betting operators inherit these obligations when they partner with Indian banks or e-wallets, making robust KYC a legal necessity rather than a courtesy. Chargeback reduction also factors in: verified accounts with confirmed payment methods are less likely to dispute legitimate transactions, protecting the operator’s revenue and maintaining healthy relationships with payment gateways.

Indian‑Specific KYC Considerations

Indian players benefit from a well-established identity ecosystem centered on Aadhaar (biometric ID), PAN cards (tax identifier), and traditional documents like voter ID cards and passports. Aadhaar is widely accepted for both identity and address proof because it links biometric data to a unique 12-digit number, enabling instant eKYC verification through the Unique Identification Authority of India (UIDAI) API. PAN cards serve dual purposes: they prove identity and satisfy tax-reporting requirements for large winnings, making them indispensable for high-stakes bettors.

Beyond central government IDs, regional documents such as ration cards, driving licenses issued by state transport authorities, and local utility bills in Hindi or regional languages are commonly accepted for address verification. Operators typically request at least one government-issued photo ID plus a recent utility bill (electricity, water, or gas) or bank statement dated within the last three months to confirm current residence.

RBI norms emphasize data consistency: the name on your betting profile must exactly match the name on your bank account, PAN card, and any payment instrument (UPI ID, debit card, or e-wallet). Discrepancies—such as a middle initial present on your ID but missing from your profile—can trigger manual reviews or outright rejection. This strict alignment protects against money laundering but requires players to double-check spelling, initials, and formatting before submitting documents.

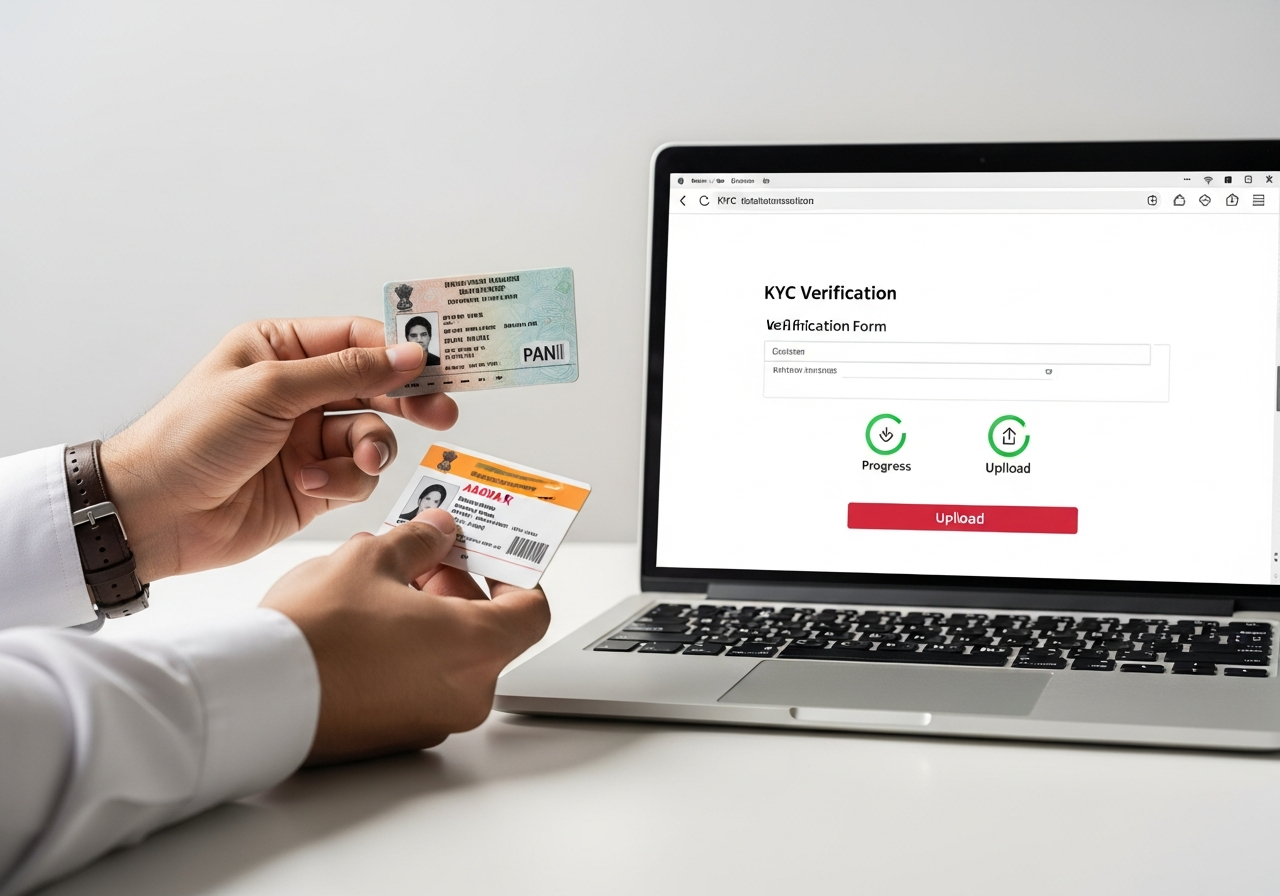

Step‑By‑Step: How To Complete KYC On An Indian Betting Site

Completing KYC involves a clear workflow that begins the moment you register and continues through document upload and payment verification. Following these steps in order minimizes errors and accelerates approval, ensuring you can place bets and withdraw winnings without unnecessary delays.

First, create your account by providing accurate personal details—full legal name, date of birth, residential address, mobile number, and email. Use the exact spelling and format that appears on your government-issued ID; even minor differences can cause automated checks to fail. Next, verify your mobile number and email via one-time passwords (OTPs) sent by the platform. Keep your phone nearby during registration to receive and enter these codes promptly.

- Register and fill your profile: Enter your full name (as on PAN or Aadhaar), date of birth (DD/MM/YYYY format), complete address with PIN code, mobile number, and email. Ensure no typos or abbreviations.

- Verify contact details via OTP: Check SMS and email for OTP codes, enter them within the validity window (usually 5–10 minutes), and confirm that both channels are active.

- Upload identity proof: Scan or photograph your Aadhaar card (front and back), PAN card, voter ID, or passport. Ensure all four corners are visible, text is legible, and there is no glare or shadow obscuring details.

- Submit address proof: Provide a recent utility bill (electricity, water, gas), bank statement, or Aadhaar card if it shows your current address. The document must be dated within the past three months.

- Verify payment method: Link your bank account or UPI ID by making a small test deposit, or upload a masked screenshot of your debit card (showing only the last four digits and your name). Some platforms auto-verify UPI during your first deposit.

- Complete liveness or selfie check: If prompted, take a selfie holding your ID next to your face, or record a short video following on-screen instructions (turn your head, blink, read a code aloud).

- Wait for review and track status: Check your account dashboard or email for verification updates. Most operators provide a status tracker showing “Pending,” “Under Review,” or “Approved” for each document type.

Throughout the process, keep your registered mobile number active to receive OTPs for additional authentication steps. If the site requests re-upload due to image quality or missing corners, act quickly—delays can extend approval times by several days.

Alternative Ways To Submit KYC (App, Web, Email, Video)

Modern Indian betting platforms offer multiple channels for KYC submission, giving you flexibility based on convenience and device availability. The most common methods are in-app upload (via iOS or Android apps), web-based upload through the desktop site, email submission to a dedicated verification address, and live video KYC conducted over a video call with support staff.

In-app and web uploads are the fastest and most secure: you navigate to the “Account” or “Verification” section, select the document type, and use your phone camera or file picker to upload scans. These portals typically enforce file-size limits (2–5 MB per image) and accepted formats (JPEG, PNG, PDF), automatically rejecting oversized or unsupported files. Encryption in transit (HTTPS/TLS) protects your documents from interception, and reputable operators store uploads in secure, access-controlled servers.

Email-based submission is useful if the app or website experiences technical issues. Look for official support addresses (e.g., [email protected] or [email protected]) listed in the site’s help section, attach clear scans as PDFs or high-resolution JPEGs, and include your account username or registered email in the subject line. Always verify the recipient address to avoid phishing scams—fraudulent emails may mimic official domains to steal your documents. Video KYC, increasingly popular for high-value accounts, involves a scheduled video call where an agent visually inspects your original ID and asks you to perform liveness checks (nod, smile, show both sides of the card). This real-time method reduces forgery risk but requires a stable internet connection and a quiet environment.

Required Documents For Indian KYC (Identity, Address, Funds)

Indian betting sites categorize KYC requirements into identity and age verification, proof of address, proof of payment method, and source of funds. Each category maps to specific document types, and operators typically specify exactly when and where to submit them. The table below outlines the core requirements, accepted Indian documents, key conditions for acceptance, and the typical trigger point for each request.

| KYC Requirement | Typical Indian Documents | Key Conditions | When It Is Asked |

|---|---|---|---|

| Identity & Age Proof | Aadhaar card, PAN card, Voter ID, Passport, Driving License | Must show photo, full name, DOB; name must match profile exactly | At registration or first withdrawal |

| Proof of Address | Utility bill (electricity/water/gas), Bank statement, Aadhaar with address, Rent agreement | Dated within last 3 months; address must match profile PIN code and city | First withdrawal or when deposit exceeds threshold |

| Proof of Payment Method | Masked debit/credit card screenshot, UPI transaction confirmation, Bank account statement | Card: show last 4 digits and name only (mask middle numbers); UPI: show VPA and name | After first deposit or withdrawal request |

| Source of Funds (if requested) | Salary slips (last 3 months), Bank statements (6 months), Tax returns (ITR), Business income proof | Required for large deposits (>₹50,000–₹1,00,000); must show regular income or savings | When cumulative deposits exceed site threshold or AML flag triggered |

| Selfie / Liveness Check | Selfie holding ID, Video recording performing gestures, Live video call with support | Face must match ID photo; no filters, good lighting, ID text readable | Random during registration or mandatory at first withdrawal |

Identity verification anchors the entire KYC process. Without a government-issued photo ID confirming you are over 18, no reputable Indian betting site will allow deposits or gameplay. Address proof ensures you reside in a jurisdiction where online betting is accessible and that your account cannot be used for cross-border money laundering. Payment-method verification ties your funding source to your verified identity, preventing third-party deposits and reducing chargeback fraud. Source-of-funds checks, though less common for casual players, become mandatory for high rollers or accounts flagged by automated AML systems; they confirm that deposited rupees originate from legitimate income rather than illicit activities.

Identity & Age Verification For Indian Players

Indian operators accept a range of photo IDs, each with specific strengths. Aadhaar cards are preferred for their biometric linkage and instant eKYC capability, allowing sites to verify authenticity via UIDAI APIs in real time. PAN cards are essential for tax compliance and often required alongside Aadhaar to satisfy both identity and income-reporting obligations. Other widely accepted documents include:

- Aadhaar card (front and back): 12-digit unique ID with photo, name, DOB, and address; enables instant digital verification if you provide your Aadhaar number and OTP consent.

- PAN card: Permanent Account Number issued by the Income Tax Department; shows name, DOB, father’s name, and photo; critical for tax reporting on large winnings.

- Voter ID card: Election Commission-issued ID with photo, name, and address; widely recognized but lacks biometric backend, so manual review may take longer.

- Passport: National or international travel document with photo, full name, DOB, and address page; highest trust level but requires uploading both photo page and address page.

- Driving License: State transport authority-issued license with photo, name, DOB, and address; less common for betting KYC but accepted by many platforms.

Consistency is paramount: the name on your chosen ID must exactly match your betting profile and bank account. Middle initials, maiden names, and spelling variations (e.g., “Kumar” vs. “Kumaar”) can cause automated checks to fail, triggering manual review and delays. Always use your full legal name as it appears on the ID when registering, and if you’ve recently changed your name (marriage, legal deed poll), update your government IDs before submitting KYC.

Proof Of Address, Payment Method & Source Of Funds

Proof of address establishes your current residential location, which operators use to confirm you are in a region where their services are legally accessible and to comply with RBI customer-due-diligence norms. Acceptable documents include electricity, water, or gas bills issued within the last three months and showing your full name and complete address including PIN code. Bank statements (savings or current account) from the past three months also serve dual purposes: they prove address and can verify your linked payment method if the same account is used for deposits.

If your Aadhaar card already reflects your current address, it alone may satisfy both identity and address requirements, streamlining the process. Rent agreements or leave-and-license contracts, notarized or registered with local authorities, are accepted by some platforms, though you may need to provide a recent utility bill in the landlord’s name plus the agreement to prove occupancy. Regional or Hindi-language documents are generally acceptable as long as the address is clearly legible; if necessary, operators may request an English translation or manual review.

Payment-method verification involves uploading a masked screenshot of your debit or credit card or confirming ownership of a UPI virtual payment address (VPA). For cards, show only the first six and last four digits, your name as embossed on the card, and the expiry date—completely obscure the middle eight digits to protect against fraud. If you deposit via UPI, a screenshot of a successful transaction showing your VPA (e.g., yourname@bankname) and registered mobile number is usually sufficient. Bank account verification can be done by making a small test deposit (₹10–₹100) initiated by the operator and confirming receipt in your statement, or by uploading a recent statement that displays your account number, IFSC code, and account holder name matching your profile.

Source-of-funds documentation is requested primarily for accounts with large or frequent deposits. Operators may ask for the last three months of salary slips, six months of bank statements showing regular income credits, filed income tax returns (ITR), or business income proof such as audited financial statements or GST returns. These checks align with Prevention of Money Laundering Act (PMLA) requirements and help platforms demonstrate to regulators that player funds are legitimate. If you receive such a request, respond promptly with clear, unredacted documents to avoid account suspension.

How To Prepare & Upload Your KYC Documents Correctly

Proper document preparation dramatically reduces rejection rates and speeds approval. Follow these best practices to ensure your scans or photos meet operator standards and pass automated quality checks on the first attempt.

- Use high resolution and good lighting: Scan documents at 300 DPI or higher, or photograph them in bright, natural light. Avoid shadows, glare from overhead lamps, and reflections that obscure text or holograms.

- Show all four corners: Capture the entire document within the frame—cropped edges or missing corners trigger automatic rejection because validation algorithms check for standard ID dimensions and security features.

- Avoid glare and blur: Hold your phone steady or use a scanner; blurry images with unreadable text cannot be verified. Remove plastic sleeves or lamination covers that cause reflections.

- Submit valid, unexpired documents: Check expiry dates on passports, driving licenses, and even Aadhaar (though Aadhaar itself does not expire, ensure your card is the latest version). Expired IDs are automatically rejected.

- Ensure name consistency across all documents: Double-check that your name on the ID, bank account, and betting profile match character-for-character, including middle initials and surname order.

- Save files in accepted formats and sizes: Most platforms accept JPEG, PNG, or PDF files under 5 MB per upload. Compress oversized images without sacrificing legibility, or split multi-page PDFs if necessary.

- Label files clearly (if emailing): Use descriptive filenames like “AadhaarCard_Front.jpg” or “PAN_Card.pdf” to help support staff quickly identify and process your documents.

Before uploading, review each file on your computer or phone screen at full size. Zoom in to verify that ID numbers, dates, and security features (holograms, watermarks) are clearly visible. If any detail is illegible or obscured, retake the scan or photo immediately. A few extra minutes spent on quality control can save days of back-and-forth with support teams.

Selfie, Video & Liveness Verification Steps

Liveness checks confirm that the person submitting documents is physically present and matches the photo on the uploaded ID, guarding against synthetic identity fraud and account takeovers. Common liveness methods include holding your ID card next to your face while taking a selfie, recording a short video where you move your head left and right or blink on command, and participating in a live video call with a verification agent.

For selfie-based checks, operators typically require you to hold your Aadhaar, PAN, or passport beside your cheek so both your face and the ID photo are visible in a single frame. Ensure good lighting on your face, remove sunglasses or heavy makeup that might obscure features, and avoid filters or editing apps—these can trigger automated fraud alerts. Some platforms use facial recognition algorithms to compare your selfie against the ID photo, flagging mismatches for manual review.

Video liveness tests involve on-screen prompts such as “Turn your head to the left,” “Smile,” “Blink twice,” or “Read this four-digit code aloud.” These dynamic actions are difficult for pre-recorded videos or static photos to replicate, providing higher assurance that a real person is completing the verification. Follow instructions carefully, ensure your face remains well-lit and centered in the camera frame, and complete the sequence in one take if possible. Live video calls with support staff are the most secure but also the most time-consuming; you’ll need a stable internet connection, a quiet environment, and your original physical IDs on hand to show both sides and any security features upon request.

KYC Limits, Timelines & What Happens After Submission

Your KYC status directly impacts what you can do on a betting platform, from deposit and withdrawal limits to the speed of fund transfers. Understanding these tiers helps you plan when to submit documents and what to expect at each verification stage.

| KYC Status | Typical Account Limits | Allowed Actions | Review Time (Approx.) |

|---|---|---|---|

| Unverified (Email/Phone OTP only) | Deposits: ₹5,000–₹10,000 max; Withdrawals: Blocked or ₹0 | Browse markets, place small bets; cannot withdraw winnings | Instant (OTP verification) |

| Partial KYC (ID uploaded, pending review) | Deposits: ₹25,000–₹50,000; Withdrawals: ₹10,000–₹25,000 | Place bets, request small withdrawals; may face processing delays | 12–48 hours (business days) |

| Full KYC (All documents approved) | Deposits: ₹1,00,000+; Withdrawals: ₹50,000–₹2,00,000 per transaction | Unrestricted betting, fast withdrawals (same-day to 24 hours), VIP perks | 24–72 hours (may be instant with Aadhaar eKYC) |

| Enhanced Due Diligence (Source of funds verified) | Deposits: Unlimited or ₹5,00,000+; Withdrawals: ₹5,00,000+ per transaction | High-stakes betting, priority support, dedicated account manager | 3–7 days (manual compliance review) |

Unverified accounts allow basic exploration and small deposits but block withdrawals entirely or cap them at negligible amounts, effectively locking your winnings until you complete KYC. Partial verification—where you’ve uploaded documents but they’re still under review—grants modest limits and slower processing. Full KYC approval removes most restrictions, enabling same-day or next-day withdrawals and access to premium features like higher betting stakes and personalized bonuses. Enhanced due diligence, reserved for high rollers depositing lakhs of rupees, requires additional income verification but unlocks VIP treatment and near-instant large-value transfers.

How Long KYC Takes & How To Track Status

Processing times vary by operator, verification method, and submission quality. Aadhaar eKYC, when available, can complete in minutes: you enter your 12-digit Aadhaar number, authorize UIDAI to share your details via OTP, and the platform instantly receives your name, DOB, and address. Manual document review typically takes 24 to 48 hours on business days, though complex cases—mismatched names, low-quality scans, or AML flags—may extend to 72 hours or longer.

Most sites provide a real-time status tracker in the account dashboard, displaying “Pending,” “Under Review,” “Approved,” or “Rejected” for each document category. Email notifications alert you when documents are approved or if re-submission is needed. If your status remains “Under Review” beyond the advertised timeframe, check your spam folder for operator emails, ensure you haven’t missed any requests for additional information, and consider contacting live chat or support email for an update.

To expedite the process, submit all required documents in a single session rather than piecemeal, respond immediately to any clarification requests, and avoid submitting during weekends or public holidays when verification teams may have reduced staffing. If you’re using video KYC, schedule your call during business hours to avoid wait times.

What Unlocks After Full Verification

Completing full KYC transforms your betting experience. Approved accounts enjoy significantly higher deposit and withdrawal limits—often jumping from ₹10,000 to ₹1,00,000 or more per transaction—enabling you to take advantage of large betting opportunities on major cricket matches, IPL finals, or international tournaments. Withdrawal processing accelerates: verified players commonly receive funds within 24 hours, whereas unverified or partially verified accounts may wait days or face manual holds.

Additional perks include eligibility for loyalty programs, cashback offers, and reload bonuses that require verified status to prevent bonus abuse. Customer support teams prioritize verified accounts, offering faster response times and dedicated assistance for high-value queries. Some platforms unlock premium features such as live streaming of matches, in-play betting with real-time odds updates, and access to exclusive markets or early-bird promotions. Finally, a verified account provides peace of mind: you’ve met all regulatory requirements, reducing the risk of sudden account freezes or forfeited winnings due to compliance issues.

Common KYC Problems On Indian Betting Sites & How To Fix Them

Even with careful preparation, KYC submissions can be rejected or delayed. Recognizing common pitfalls and knowing how to correct them saves time and frustration, ensuring your account reaches verified status as quickly as possible.

- Name mismatch between profile and ID: If your betting profile shows “Rajesh K. Sharma” but your Aadhaar reads “Rajesh Kumar Sharma,” automated checks will fail. Fix: Update your profile to match your ID exactly, or submit a name-change affidavit if you legally changed your name after obtaining the ID.

- Blurry or incomplete scans: Photos with missing corners, illegible text, or excessive glare are automatically rejected. Fix: Retake the image in good lighting, ensure all four corners are visible, and verify text readability before uploading.

- Expired or outdated documents: Passports, driving licenses, or utility bills older than three months are invalid. Fix: Renew expired IDs or request a fresh utility bill, then upload the updated version.

- Address mismatch: Your profile address reads “Mumbai, Maharashtra 400001” but your utility bill shows “Navi Mumbai, Maharashtra 400614.” Fix: Either update your profile address to match the bill or provide a different proof-of-address document reflecting your registered location.

- Masked payment details unclear: If you obscure too much of your card or UPI screenshot, the operator cannot confirm ownership. Fix: Show the first six and last four card digits clearly, along with your name; for UPI, ensure your VPA and registered mobile number are visible.

- Selfie does not match ID photo: Significant changes in appearance (new beard, different hairstyle, weight loss/gain) or poor lighting can cause facial recognition to fail. Fix: Retake the selfie in bright, even lighting with a neutral expression, and if necessary, contact support to request manual review by a human agent.

- Third-party document submission: Uploading a family member’s utility bill or using someone else’s bank account for deposits violates KYC rules. Fix: Provide documents in your own name only; if you share a household, obtain a bill or statement that lists you as the account holder or co-holder.

When a document is rejected, operators typically send an email or in-app notification explaining the reason. Read these messages carefully, address the specific issue cited, and resubmit corrected files as soon as possible. Avoid uploading the same rejected document repeatedly without changes—this can flag your account for manual review or even trigger a temporary lock.

When To Contact Support Or Escalate

If your KYC remains “Under Review” for more than three business days with no communication, or if you receive a rejection notice you believe is incorrect, reach out to the operator’s support team via live chat, email, or phone. Provide your account username or registered email, a brief description of the issue, and any relevant reference numbers from previous correspondence.

Keep detailed records of all KYC submissions: save copies of uploaded documents, screenshot confirmation emails, and note the date and time of each upload. If support requests additional documents or clarification, respond within 24 hours to prevent further delays. For persistent issues—such as repeated rejections despite correct documents—ask to escalate your case to a senior compliance officer or KYC specialist who can perform a manual review.

In rare cases where an operator’s KYC process appears unreasonably obstructive or you suspect your documents are being mishandled, consider filing a complaint with the platform’s licensing authority (if offshore and regulated) or seeking advice from consumer forums and online gambling watchdog sites. However, most issues resolve through clear communication and prompt resubmission of corrected documents.

No‑KYC & Low‑KYC Betting Options For Indian Players

While the majority of reputable Indian betting sites enforce full KYC, a subset of platforms—often offshore or cryptocurrency-based—offer reduced or no-KYC onboarding. Understanding the trade-offs between convenience and security helps you make informed decisions about where to place your bets.

| Type of Site | KYC Level | Typical Payment Methods | Main Pros | Key Risks |

|---|---|---|---|---|

| Fully Regulated (Curacao, Malta, UKGC) | Full KYC (ID + address + funds) | INR bank transfer, UPI, e-wallets (Paytm, PhonePe), cards | Legal protection, dispute resolution, fast verified withdrawals | Longer onboarding; must share personal data |

| Low-KYC Offshore | Email + phone only; KYC on large withdrawals | Crypto (BTC, USDT), some e-wallets | Quick signup, partial anonymity, flexible limits initially | Sudden KYC demands when cashing out; weaker legal recourse |

| No-KYC Crypto Sites | None (wallet address only) | Bitcoin, Ethereum, USDT, other cryptocurrencies | Maximum privacy, instant deposits/withdrawals, no ID required | No regulatory oversight; if funds are seized, little legal remedy; vulnerable to scams |

Fully regulated platforms prioritize player protection and compliance, requiring comprehensive KYC in exchange for robust dispute resolution, licensed game fairness, and guaranteed payouts. Low-KYC offshore sites allow basic play with minimal verification but reserve the right to request full documents before processing large withdrawals—a practice that can surprise players who assumed they were truly anonymous. No-KYC crypto betting sites offer the highest degree of privacy, accepting only cryptocurrency deposits and relying on blockchain transparency rather than identity checks. While this appeals to privacy-conscious bettors, it also means zero consumer protection: if the operator vanishes or disputes your win, you have no licensing authority to appeal to.

Why Most Serious Sites Still Enforce Full KYC

Reputable operators enforce full KYC to meet anti-money laundering (AML) and combating the financing of terrorism (CFT) obligations under international and local regulations. Licensing bodies such as the Malta Gaming Authority, UK Gambling Commission, and Curacao eGaming mandate identity verification to prevent underage gambling, detect fraud, and trace illicit funds. For sites accepting Indian rupee deposits via bank transfer or UPI, RBI guidelines further require customer due diligence to align with Know Your Customer norms applied to financial institutions.

Beyond regulatory compliance, KYC reduces operational risks. Verified accounts lower chargeback rates—players cannot dispute legitimate transactions by claiming their card was stolen—and improve payment-processor relationships, which in turn supports faster, more reliable deposits and withdrawals. Operators also use KYC data to identify problem gamblers, enforce self-exclusion programs, and prevent bonus abuse by detecting multi-accounting or identity theft.

For players, this rigor translates to trustworthiness. A platform that invests in robust KYC infrastructure signals commitment to fair play and responsible gambling, providing confidence that your winnings will be paid out and disputes handled transparently. While the initial verification may feel intrusive, it ultimately protects your funds and personal information far better than unregulated alternatives.

When Low‑KYC Might Be Used & Practical Precautions

Some bettors prefer low-KYC or no-KYC options for privacy reasons, to avoid sharing sensitive documents like Aadhaar or PAN, or to test a new platform before committing to full verification. Cryptocurrency-only sites also appeal to users who value financial sovereignty and wish to keep betting activity separate from traditional banking records.

- Testing a platform: Use low-KYC sites to explore game selection, user interface, and customer support with a small deposit before deciding whether to submit full KYC on a regulated alternative.

- Privacy concerns: If you’re uncomfortable sharing government IDs due to data-breach fears, crypto-based no-KYC sites provide an option—though you sacrifice legal recourse and regulatory oversight.

- Jurisdictional restrictions: Players in regions with ambiguous online-gambling laws may choose offshore low-KYC platforms to maintain a degree of anonymity, though this carries legal and financial risks.

Practical precautions when using low- or no-KYC platforms include keeping balances small (deposit only what you can afford to lose entirely), conducting test withdrawals early to confirm the site honors payouts without surprise KYC demands, researching operator reputation on independent forums and review sites, using separate crypto wallets to isolate betting funds from long-term holdings, and never depositing large sums or high-value documents (if any KYC is eventually requested) without verifying site authenticity. Remember that no-KYC sites can impose sudden verification requirements or freeze accounts at any time, leaving you with limited appeal options.

Security, Privacy & Best Practices For KYC On Indian Betting Sites

Submitting personal documents online always carries privacy risks, but following security best practices minimizes exposure to data breaches, identity theft, and phishing scams. Protecting your KYC information is as critical as the verification itself.

- Verify site authenticity before uploading: Confirm the betting platform’s URL matches its official domain (look for HTTPS and a valid SSL certificate). Avoid clicking links in unsolicited emails; navigate directly to the site by typing the address into your browser.

- Use secure, private networks: Never upload KYC documents over public Wi-Fi at cafes, airports, or hotels. Use your home network or a trusted mobile data connection to prevent interception by malicious actors.

- Enable two-factor authentication (2FA): Activate 2FA on your betting account using an authenticator app (Google Authenticator, Authy) or SMS codes. This adds a second layer of protection even if your password is compromised.

- Check for encryption: Ensure the upload portal uses HTTPS encryption (look for a padlock icon in your browser’s address bar). Reputable operators encrypt documents both in transit and at rest in secure servers.

- Beware of phishing emails: Fraudsters may send fake KYC requests that mimic official operator branding. Verify sender email addresses carefully, look for spelling errors or generic greetings, and contact support via official channels if an email seems suspicious.

- Limit file sharing: Upload documents only through official site portals or verified email addresses listed in the platform’s help section. Never share Aadhaar or PAN via social media, unencrypted messaging apps, or third-party file-sharing services.

- Monitor account activity: Regularly review your betting account’s transaction history and login logs. Report any unrecognized activity to support immediately and change your password.

Operators are required to store KYC data securely and limit access to authorized compliance personnel. Reputable platforms comply with data-protection standards such as GDPR (for international players) or India’s Information Technology Act, employing encryption, access controls, and regular security audits. Before submitting documents, review the site’s privacy policy to understand how your data will be used, whether it will be shared with third parties, and your rights to request data deletion after account closure.

Maintaining Your Verified Status Over Time

KYC is not a one-time event. As your personal circumstances change—moving to a new address, renewing an expired passport, changing your name through marriage or legal process—you must update your betting account to maintain verified status and avoid withdrawal delays.

Set calendar reminders to check the expiry dates of uploaded documents, especially passports and driving licenses, and proactively upload renewed versions before they expire. If you move house, update your profile address and submit a new utility bill or bank statement reflecting the new location within 30 days. Failure to do so can result in mismatched address checks during future withdrawals, triggering manual review or temporary account holds.

Some operators conduct periodic re-verification, especially for high-value accounts, requesting updated proof of address or source of funds every 12 or 24 months. Respond promptly to these requests to avoid service interruptions. Keeping your contact details current—mobile number and email—ensures you receive timely notifications about verification renewals or security alerts.

Quick KYC Checklist For Indian Bettors

Follow this streamlined checklist to complete KYC efficiently and avoid common delays. Each step builds on the previous one, ensuring a smooth path from registration to verified, withdrawal-ready status.

- Register with accurate profile details: Enter your full legal name (as on Aadhaar or PAN), correct date of birth, complete residential address with PIN code, active mobile number, and email. Double-check spelling and formatting.

- Verify mobile and email via OTP: Respond to OTP messages and emails immediately to activate your account and enable communication channels for future KYC updates.

- Gather required documents before upload: Collect scans or high-resolution photos of your Aadhaar card (or PAN, passport, voter ID), a recent utility bill or bank statement (within 3 months), and payment-method proof (masked card screenshot or UPI confirmation).

- Upload documents in one session: Submit all required files together to expedite review. Ensure each image is clear, shows all four corners, and meets file-size and format requirements (JPEG/PNG/PDF, under 5 MB).

- Complete selfie or liveness check: If prompted, take a well-lit selfie holding your ID next to your face, or follow on-screen video instructions (turn head, blink, read code). Avoid filters and ensure your face and ID photo are clearly visible.

- Track verification status daily: Monitor your account dashboard for status updates and check email (including spam folder) for operator messages. Respond to any re-upload or clarification requests within 24 hours.

- Test a small withdrawal after approval: Once fully verified, initiate a small test withdrawal (₹500–₹1,000) to confirm your bank details are correctly linked and the payout process works smoothly before placing larger bets.

Submitting KYC immediately after registration—rather than waiting until your first withdrawal—eliminates last-minute stress and ensures you can access your winnings without delay. Many platforms process documents faster when there is no pending withdrawal, as compliance teams prioritize active payout requests.

Final Tips To Avoid KYC Delays On Indian Betting Sites

Consistency is the golden rule: ensure your name, date of birth, and address match exactly across your betting profile, government IDs, bank account, and payment instruments. Even a single-character discrepancy—such as “Singh” vs. “Simgh”—can trigger automated rejections and manual reviews that add days to approval times.

Respond promptly to operator queries. If support requests additional documents or clarification, treat it as urgent and reply within hours, not days. Keep digital and physical copies of all submitted documents so you can quickly resend or provide supplementary proof if needed. Finally, choose reputable, licensed platforms with transparent KYC policies and responsive customer support; investing time in research upfront saves frustration and protects your funds in the long run.